A full decade since the first retail stores fell victim to the inexorable march of ecommerce and Amazon Inc. (NASDAQ:AMZN), the retail apocalypse shows no signs of abating. The last decade has been brutal to the American retail industry, as countless traditional malls continue to shutter at record highs. Last year alone, a total of 17 major retailers, including icons such as Payless, Charming Charlie and Gymboree, filed for bankruptcy with more than 9,500 stores closing shop.

The carnage has continued in the current year, with the coronavirus outbreak triggering unprecedented inventory and liquidity headwinds forcing even more stores to shut down.

The year kicked off with the parent of fine paper specialist Papyrus quietly going into liquidation before eventually filing for bankruptcy. A torrent was to soon follow, with 27 major retailers joining the expanding retail graveyard in the year-to-date. These include industry bellwethers such as giant department store chain JCPenney (NYSE:JCP), luxury department store operator Neiman Marcus and famous New York discount store chain, Century 21.

And now yet another potent force has emerged to put even more pressure on the battered sector: Direct-to-consumer (DTC) brand movement.

At a time when brick-and-mortar are struggling mightily with sharp declines in foot traffic, sales and profits, the DTC space has continued to flourish and even record double-digit growth amid the pandemic.

Not surprisingly, DTC stocks have been shooting the lights out, with Overstock.com Inc. (NASDAQ:OSTK) managing to reverse years of losses to power up 874% YTD; Wayfair Inc. (NYSE:W) is up 229% while Shopify Inc. (NYSE:SHOP) has gained 161% over the timeframe.

Interestingly, no mainstream online company has folded.

Source: CNN Money

The retail apocalypse

It’s not by accident that the ever-growing wave of retail store closures has coincided with the ecommerce explosion.

Over the past decade, North American and global consumers have shifted their purchasing habits quite dramatically thanks to the meteoric rise of digital shopping.

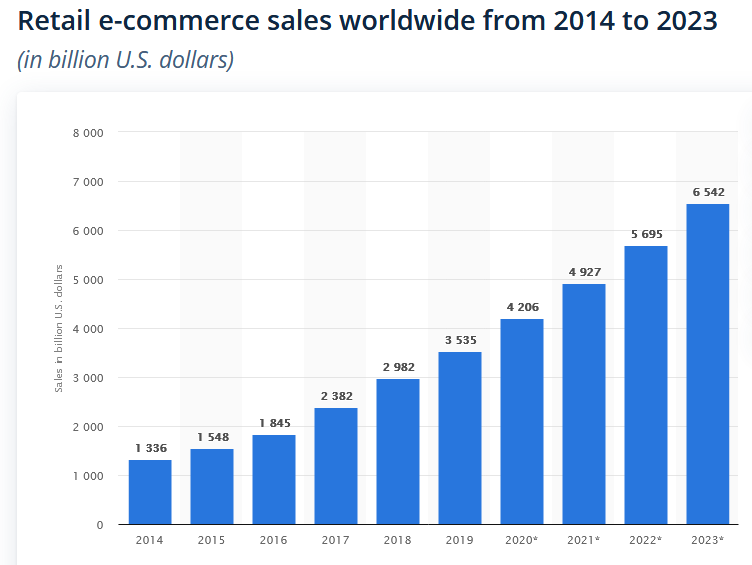

Online sales have been growing much faster than brick-and-mortar sales, climbing nearly 400% to $6.5 trillion in the 2014-2020 period.

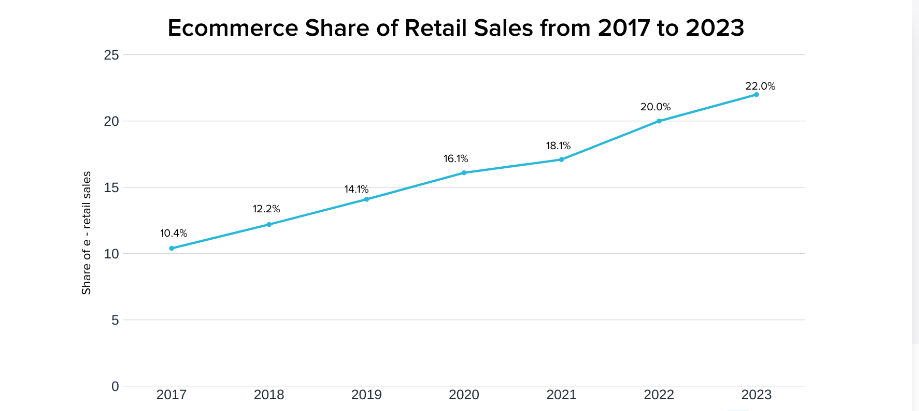

According to eMarketer, ecommerce sales as a share of retail have climbed from 10.4% in 2017 to 16.1% in 2020. That trend is expected to hold over the next decade with digital sales projected to grow to 22% of total retail sales by 2023.

Source: Statista

Source: eMarketer

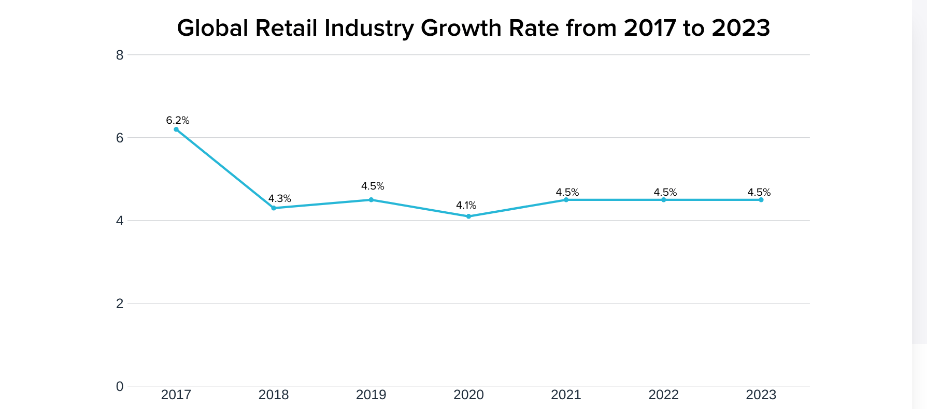

In contrast, retail sales growth has gone through a slump, falling from 6.2% in 2017 to 4.1% in the current year, with the lackluster growth expected to continue over the coming years.

Source: eMarketer

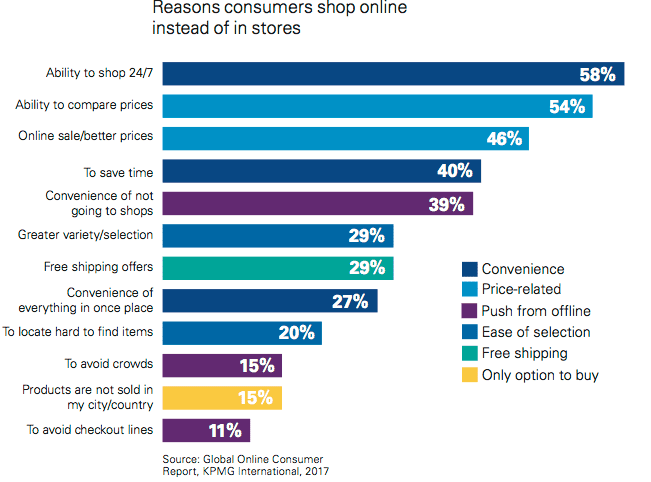

A big reason for the ecommerce megatrend going on a tear can be chalked up to convenience.

Online shopping allows the customer to:

- Shop 24/7

- Avoid crowds and save time

- Easily compare prices between different sellers

- Enjoy better prices compared to brick-and-mortar stores

- Enjoy expedited delivery with many companies offering same-day deliveries

- Enjoy better variety

Source: Smart Insights

A forensic analysis of this year’s high-profile retail closures proves that brick-and-mortar stores are likely to continue taking a backseat to their digital brethren.

Take Century 21, for instance. For more than six decades, the company has been a favorite retailer especially among New Yorkers, managing to survive even after its downtown flagship was destroyed in the 9/11 terrorist attacks.

Century 21 was an early entrant in the off-price game, focussing on selling high-end apparel for savvy fashionistas. But unlike peers TJX Companies Inc.(NYSE:TJX)., Ross Stores (NASDAQ:ROST) and Burlington Stores (NYSE:BURL) which have eschewed ecommerce in favor of their defining store-based treasure hunts and also partly in a bid to protect their margins, Century 21 opened a website to help it expand beyond the four states where it operates.

Unfortunately, the company has been forced to close down after insurance companies denied it $175 million in Covid-19-related claims.

Talk about doomed if you do, doomed if you don’t. In this case, merely having an online presence has not been enough to save Century 21–and dozens others like it.

J.C. Penney’s problems go back years ago when the company went on a death spiral of falling store traffic, mounting losses and constant sales declines. But years of trying to engineer a lasting turnaround failed to bear fruit, which– coupled with a deadly pandemic–forced the 118-year old retailer to throw in the towel and file for Chapter 11 bankruptcy.

JCP failed to reinvent itself and change with the times, with its stores and merchandise roundly viewed as bland and unexciting. Even more perplexing is that the company failed to build on its early lead as one of retail’s online shopping pioneers. JCP was once regarded as an online stalwart, with digital sales exceeding $1 billion by 2006. But ultimately its brick-and-mortar stores proved too much of a drag, and now the company plans to shutter 242 of its 846 nationwide stores by the end of 2021.

Neiman Marcus has been forced to pay the price after falling into an all-too common business trap–taking on too much debt. Two rounds of private equity buyouts left it saddled with a mountain of debt making it really difficult for the retailer to keep up with rivals Nordstrom Inc. (NYSE:JWN) and even Macy’s (NYSE:M). This has been further exacerbated by the fact that the department store sector has been in the dog house for years now.

Nevertheless, the century-old Dallas-based retailer remains in a much better position than other fallen icons since it has managed to maintain fierce loyalty among some deep-pocketed customers. Further, a virtual styling service has helped boost online sales with digital sales making up 30% of total sales. The company’s Mytheresa business has survived and will continue to operate independently.

The rise of DTC

Consumers are constantly in search of convenience, and the direct-to-consumer (D2C) model offers them precisely that.

A new generation of disruptive brands have been shaking up retail, with direct-to-consumer e-commerce companies building, marketing, selling, and shipping their products themselves without any middlemen.

Direct-to-consumer (or D2C) businesses manufacture and ship their own products directly to customers without going through traditional stores or other middlemen.This allows DTC companies to offer products at lower costs than traditional consumer brands, while at the same time maintaining end-to-end control over the making, marketing, and distribution of their products. D2C brands are able to experiment with different distribution models, from direct shipping to consumers and partnering with physical retailers to opening pop-up shops. In other words, they are not limited to traditional retail stores for exposure.

These trends have been helping D2C to expand at an even faster clip than traditional ecommerce, with eMarketer forecasting that D2C sales will hit $17.75 billion in 2020, good for 24.3% Y/Y growth.

D2C has taken over many corners of traditional retail, with once tiny startups now dominating.

Casper Sleep Inc. (NYSE:CSPR), which IPOed in February, is taking on the mattress industry; Harry’s and Dollar Shave Club are taking on the razor industry; The Honest Company is upending the baby products and cleaning segment while others like Soylent are building entirely new product categories. Amazon features prominently in the (partial) distribution of these products though most have managed to carve out niches away from Amazon’s dominant marketplace.

The big boys are not to be outdone though.

Overstock, the online purveyor of home decor, furniture, home improvement, and other related products, has enjoyed a monster rally thanks to its latest push to apply the DTC model to its online home furniture business. A key trend driving Overstock’s furniture business higher is a boom in home renovations as the pandemic forces more people to work from their homes. During its latest earnings call, Overstock reported Q3 revenue of $731.65M (+110.8% Y/Y); adjusted EBITDA of $40M and Q3 GAAP EPS of $0.50 thanks to new customers more than doubling. The company says its pure play e-commerce and partner supplier dropship model are a great fit for its business and support high growth.

Shopify has been recording similar bullish trends, with the company’s GMV (Gross Merchandise Volume) rising 109% in Q3 to $30.9B thanks mainly to robust merchant revenue growth of 132% to $522.1M. Overall revenue of $767.4M (+96.5% Y/Y) and GAAP EPS of $1.54 were equally impressive. And just like Overstock, Shopify’s management has revealed that it has been recording ‘‘incredible demand’’ thanks to a ‘‘decisive shift to digital commerce.’’

DTC headwinds

Despite the incredible opportunities that D2C has been opening up for ecommerce players, the burgeoning industry is facing its fair share of challenges.

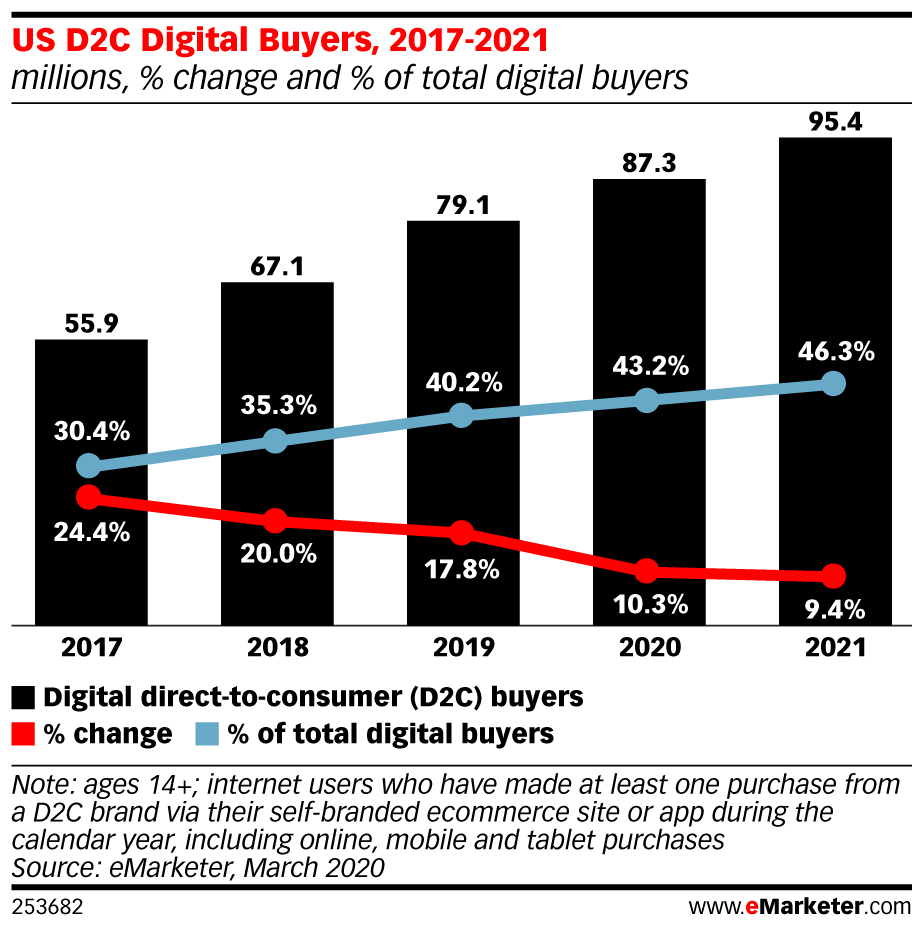

As eMarketer has noted, the same low barriers to entry that have enabled many retailers to join the fray have, unfortunately, also led to overcrowding and increased customer acquisition costs. Indeed, the analyst expects D2C buyer growth rates to slow down to single digits from 2021 after enjoying 24% growth just three years ago.

Source: eMarketer

On the opposite end of the spectrum, stronger-than-expected demand could easily overwhelm even seasoned players and potentially lead to brand damage. Good case in point is Shopify which has reportedly been struggling to keep up with a rapid increase in merchant accounts on its platform.

Despite these growing pains, Wall Street remains bullish on the D2C sector, with eMarketer projecting 87.3 million D2C eCommerce shoppers aged 14 and older in the current year in the United States alone, up 10.3% from the prior year.